Roku: Q2 Earnings

Roku: Q2 Earnings

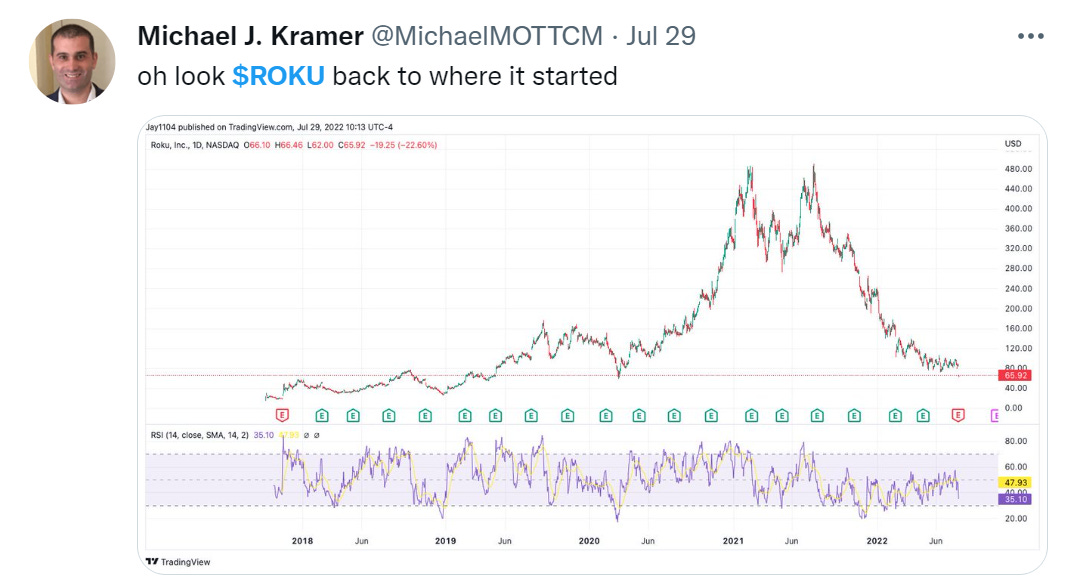

The Stock is down 23%, did something change fundamentally?

We covered Roku on our deep-dive published July 18th called “Roku: The Switzerland of the Streaming Wars” This is a short summary and an update after their Q2 earnings were announced this past week. During earnings Season we will do this short updates of the companies we have covered so far Opendoor Peloton Carvana Rivian Roku and UBER

$ROKU

Roku reported earnings this past Thursday and from the Market’s reaction you would think that the company is going out of business. Just after earnings were announced Roku was trading down close to 30% by the time the market opened the next day it opened at $66.1 it finally closed down 23%. Was this large move justified, has something changed dramatically for the business?

Performance Summary:

Revenue

Q2 Revenue was $764m vs $804 consensus estimate

Growth has continued to slow down going from 28% to 19% in the quarter.

Platform revenue grew by 26% YoY

Platform revenue increased by $140.9 million YoY. Yet this growth was slower than what the market expected. Roku in their press release explain this with the following statement: ‘’there was a significant slowdown in TV advertising spend due to the macro-economic environment, which pressured our platform revenue growth, Consumers began to moderate discretionary spend, and advertisers significantly curtailed spend in the ad scatter market (TV ads bought during the quarter)’’

Player revenue slowdown continued at the same pace of Q1 (19%)

Player revenue decreased by $21.6 million YoY

Player revenue was impacted primarily due to a decrease in both the volume of streaming players sold and the average selling prices.

The volume of streaming players sold decreased by 16% and the average selling price of players decreased by 5% driven by reductions in consumer discretionary spending, which they believe is a result of rising inflation and recessionary fears.

Roku’s guidance for Q3 came in lower than expected at $700m vs market consensus of $902m

Key Metrics:

Roku ended the quarter with 63.1 million active accounts ( 15% growth YoY)

Roku added 1.8 million active accounts in Q2 2022

Accounts grew faster in Q2 2022 than Q1 2022 (1.8m vs 1.2m) it was also higher than the accounts added in Q2 2021 (1.5m)

Roku explains that the higher net adds in the quarter despite the lower revenue from players by TV manufactures trying to dispose of inventory faster.

ARPU grew 21% YoY and now sits at $44.1

Streaming hours came down from 20.9b to 20.7b. Roku explained this as cyclical. We did see a drop in 2021 from 18.3 to 17.4b hours. The drop in hours in 2022 was better, only -1% vs -5% in 2021

Cost and Expenses:

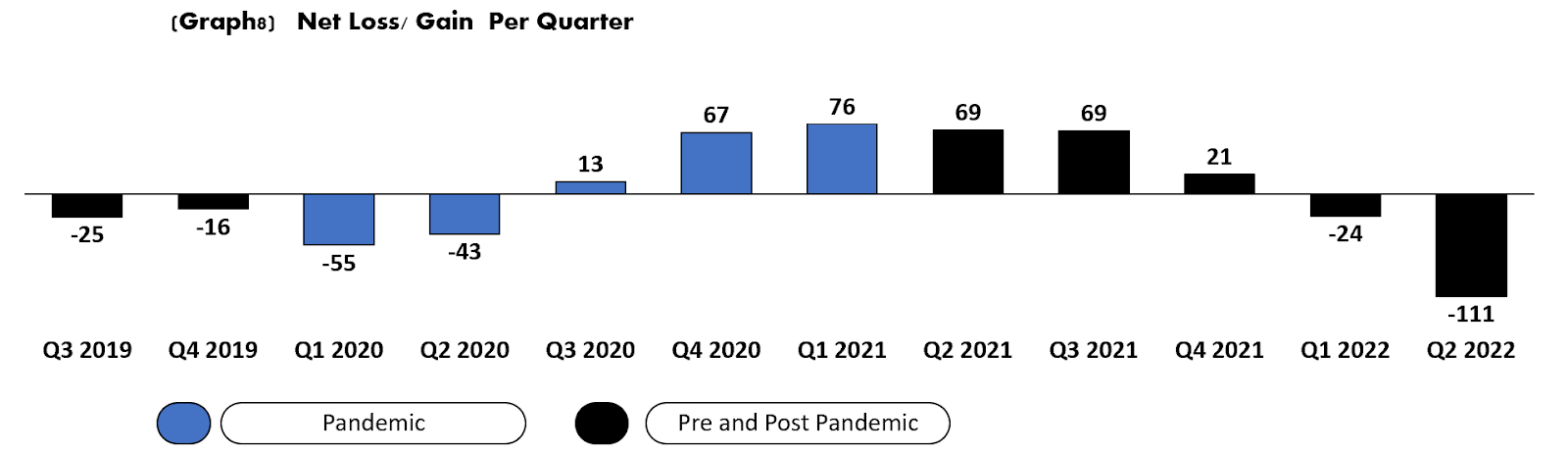

EPS was (0.82) vs (0.68) consensus estimate

Roku accelerated its losses for the quarter to $112m.

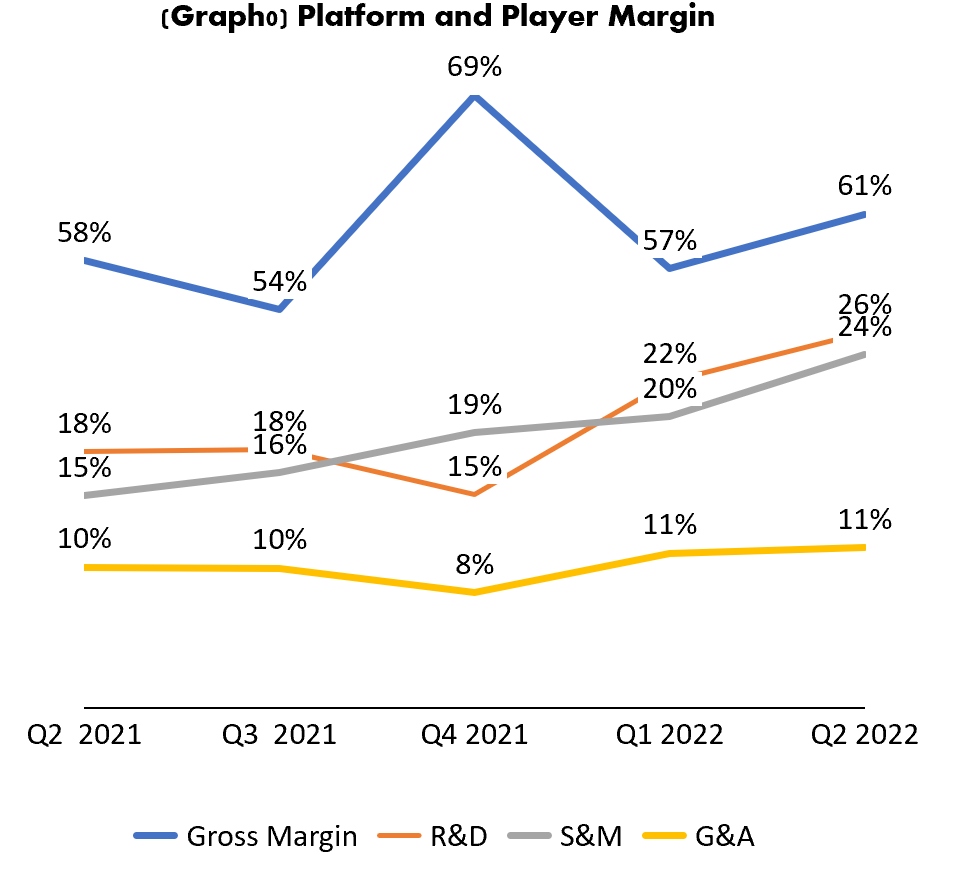

This is something that, even though it came a little above estimates, it was expected. Roku announced earlier that they would go back to invest more heavily in the growth of the platform. We can see that R&D investment went from 18% of revenue a year ago to now being 26% of revenue.

Platform Direct Cost increased and it now represents 44% of the revenue

Platform direct cost increase is primarily driven by higher cost of acquiring content

Platform direct cost also increased an additional $19.6 million (YoY) due to increases in cloud services costs for supporting the platform

Player costs continue to be above its revenue given that Roku is trying not to pass cost to customers. Cost have increased for Roku while they are trying to battle supply chain issues.

Research and development expenses increased primarily due to increases in personnel-related costs, a result of increased engineering headcount and related stock-based compensation, higher facilities and information technology

Sales and Marketing expenses increase by close to 100% when compared to Q1 2021 and by $38.5 m vs last quarter.

Sales and Marketing the increase is primarily due to increases in personnel-related costs of $44.7 million related to increased headcount in sales and sales support, product management, marketing, and business analytics to support efforts to grow our business.

Sales and marketing expenses also include an increase of $33.8 million mainly due to increases in marketing, retail and merchandising costs, and other advertising expenses to promote the Roku brand

General and Administrative increased by 35% YoY and $6m vs last quarter. The majority of the increase is related as well to an increase in headcount.

Balance Sheet

Roku had $2.05b in cash at the close of Q2 2022

Cash used for operating was $9.9m. Very low considering the amount of cash they currently hold

The company has very little liabilities and debt.

The $138.5 m in accumulated losses to date have been offset by more than $305m in non-cash charges. (Stock based compensation $156m, Depreciation and Amortization $123m, etc.)

Investing activities reduced cash by $92m, most of it in the purchase of PPE

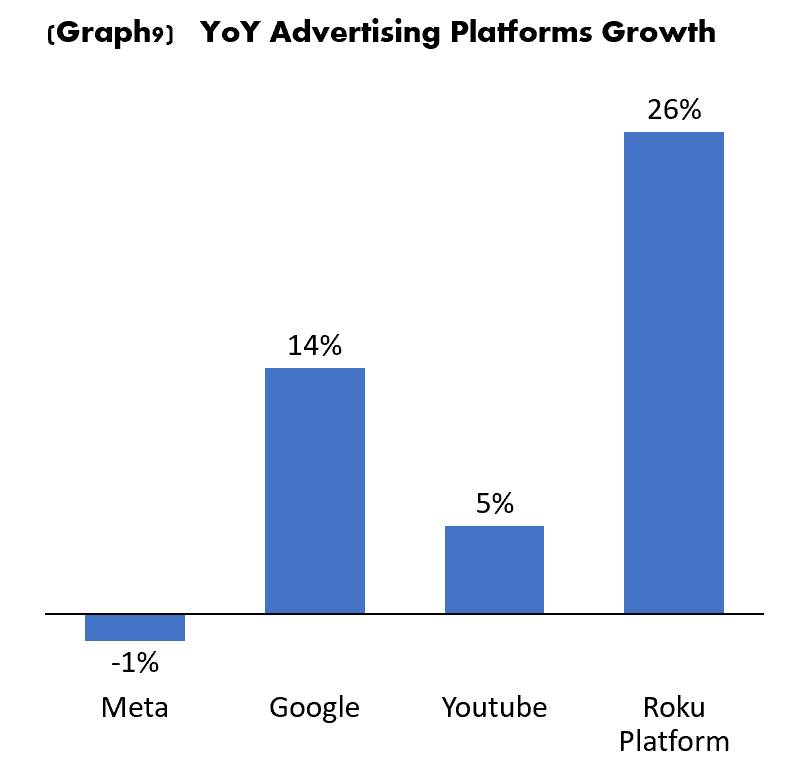

Advertising

The biggest worry from the market was the sudden and rapid slowdown of revenue in advertising for the platform side of the business. Rokus has explained this mostly as an issue of economic slowdown and the fact that advertisers are starting to cut on some of the advertising expenses.

Roku announced in their earnings release that despite the slowdown they still managed to get $1b in upfront commitments. This is a sign that the stream of revenues for Roku will continue and nothing has fundamentally changed for their business. Compared to other big advertising platforms Roku has not had a dramatic change in trend that would raise worries. Their platform is far smaller and the market would be expected to keep growing at a fast pace. But considering that the platform, for now, has only 63m active accounts, it is understandable that would be one of the places that the advertiser would cut first. (The Upfront process began in Q2 and concluded in Q3 - upfront is a gathering at the start of important advertising sales periods, its main purpose, to allow marketers to buy television commercial airtime "up front", before the television season begins)

The economic situation will get worse, not better. So this will be a hard headwind for Roku for at least the next three quarters. This has been confirmed by the low guide they gave for Q3 (looks like a very conservative guide considering the $1b in upfront the managed to get) Nothing really has changed fundamentally on their platform how they monetize advertising on it.

Market Response

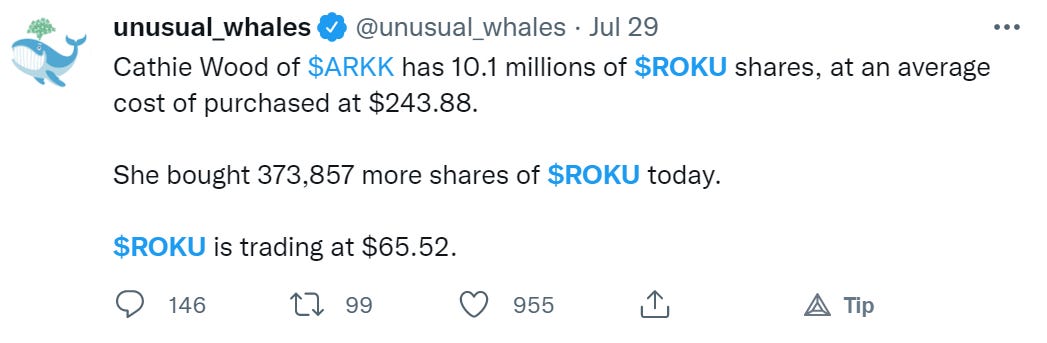

These are some of the reactions seen in the market and on twitter regarding Roku’s earnings.

Cathie Wood:

“While macroeconomic conditions could continue to weigh on Roku's short-term financial performance, our outlook for Roku's growth potential remains robust. As the #1 streaming platform by hours streamed in the US, Canada, and Mexico, Roku should continue to lead the advertising shift from linear to digital TV.”

Outlook

The TV platform business is a sound business and it is the future of TV. Content providers (Netflix, HBOMAX etc.) will need these platforms like TV channels needed Cable Providers in the past. The TV OS will be the replacement as the distributor of content, nothing has changed here. The battle for this continues to be between Amazon, Google, Roku. Roku continues to be the favorite in the US, Canada and Mexico. Yet their presence internationally is no way near the one in the US. They need to penetrate the rest of the world and they need to do it as soon as possible. Our opinion is that it is more important for them to aggressively reach international markets and become more available in TVs that are sold internationally. Even if this even means stop charging for the licensing of the OS or even paying for the benefit of being in the TVs. Samsung and LG are the TV leaders in the world. They need to get one of them, if that means paying them or giving the licensing for free it will eventually pay itself back with far better penetration of the worldwide market. Their main goal is to grow from the 63 million accounts they have, and reach the highest possible market share of the total estimated market of 1 billion streamers worldwide.

Our valuation metrics remain the same, even if the following quarters are a challenge for the company. They will be battling supply chain issues and an economic slowdown. A world in which it is more expensive to get payers to consumers, consumers want to spend less money on new players and advertisers, the first thing to cut is advertising expenses. With this environment the company seems to be heading (only in the short term) to the assumptions we took for the conservative case, in which base grew slower and ARPU remained close to flat. The result from that scenario gave us a $43.7 per share valuation, yet we don’t believe that this behavior will be longer than a few quarters so this remains a conservative case instead of becoming a base case.

Roku has to be careful in not overspending on original content. It is not the best strategy, it could be good for bringing viewers to the Roku channel, yet it is a lost battle against big content providers like Disney or Netflix. Their role is to become a platform, to become Switzerland of the Streaming wars. The role is to penetrate the world with their platform as fast as possible. We believe most of their investments should be focused towards achieving international growth and should not expand original content aggressively. The more they do international, the better their long term.

Read our Previous Pieces on:

Opendoor Peloton Carvana Rivian Roku Uber