Roku: The Switzerland of the Streaming Wars

Roku: The Switzerland of the Streaming Wars

Who is going to be the TV platform leader?

Update: Since the original publication of this article we have also published our analysis on their Q2 earnings, you can read that here: ROKU: Q2 Earnings

Roku was founded in 2002 by Anthony Wood, the name means six in Japanese, it was named like this because it was the sixth company that had been founded by Wood. It was not until 2008 that the company released their first Roku device. This was part of a partnership with Netflix that looked to allow Netflix subscribers to stream Netflix content to their TVs. From there, they have continued growing and adding many more devices and many more revenue streams. Today they are trading at $85.77 per share or $11.6b. Last year they were trading considerably higher at $490.42, they have lost 82% of its value since then, similar to other companies that have been hit hard in the past 12 months. They are trying to play in a very crowded industry, they are placed in the middle of the ‘’streaming wars’’, but perhaps its approach to the war is one of the better ones?

Business Model:

Revenue Streams:

There are two groups of revenue sources for Roku:

Platform Revenue: Platform revenue includes many sources, but Rokus does not report the details, it just gives us the revenue for the whole group. Some of the items Included in this are:

Sale of digital advertising and related services including the OneView ad platform

Content distribution services (such as subscription and transaction revenue shares, media and entertainment promotional spending, the sale of Premium Subscriptions, and the sale of branded channel buttons on remote controls)

Licensing arrangements with service operators and TV brands

How Digital advertising works:

Ads run on ad breaks during movies and TV

Ads are 15 seconds, 30 seconds and more.

They place the ads on the hundreds ad supported channels available and the Roku Channel

They show the ad only to the target audience selected by the advertiser.

First the advertiser selects the audience they want (They can choose from own data, Roku Audiences data or Marketplace Audience like Axiom and Epsilon Etc.)

Second is to choose where to run the ads. The advertiser can choose from Roku Channel, Other Media (if they have something already with publishers it can be added, it is able to consolidate broadcast, cable and streaming, also goes beyond only the Roku platform)

They offer a dedicated way to target customers and a consolidated way to manage streaming advertising investments for companies

Some of the Publishers currently using Roku are:

Paramount + , Apple TV +, HBOMAX, Peacock and BET+ and many smaller channels are looking to monetize their channel.

In summary, we would compare Roku’s advertising to Meta or Google ( and YouTube). But also to Android and IOs. Roku is trying to become the platform OS for the biggest screen in the household. It is still a highly fragmented business with many players from many backgrounds, both from software and hardware.

TV Manufacturing Partners: Some of the partners manufacturing TVs with Roku OS are:

TCL

Sharp

Hisense

Haier

Philips

Sanyo

Element

JVC

RCA

Hitachi

Magnavox

Westinghouse

Insignia

Player Revenue: The sale of streaming devices. They are currently in their Tenth generation. The devices for this generation are:

Roku Streaming Stick 4K (3820)

Roku Streaming Stick 4K+ (3821)

Roku Ultra LT (4801)

Roku Streambar Pro (9101)

Key Metrics / Performance

For 2021

Revenue was $2.76b

Net income was $242m or 8.7% of Revenue

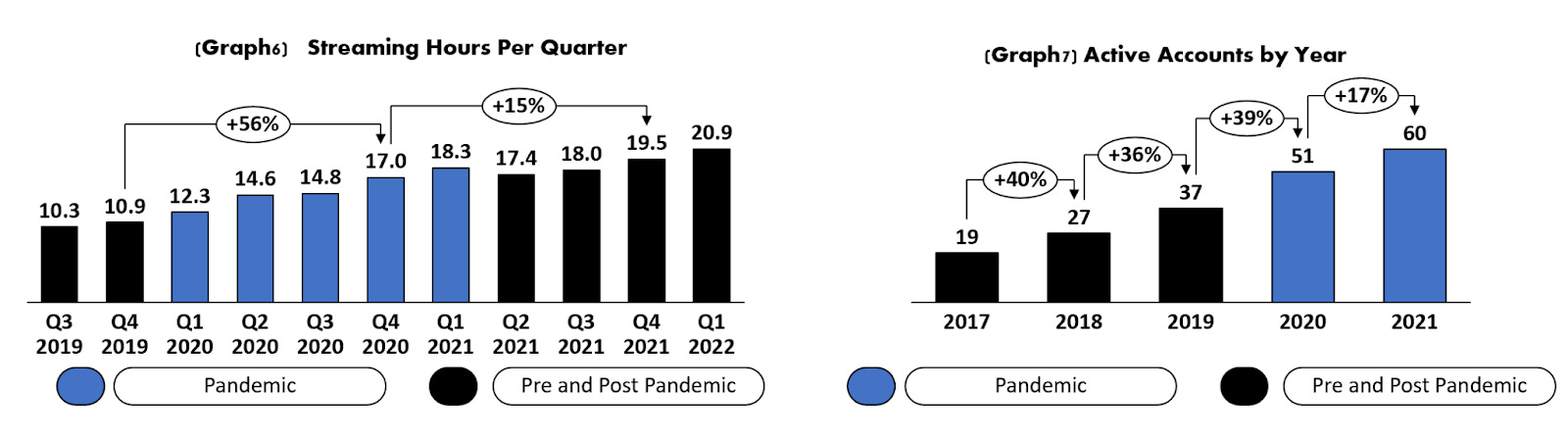

Active Accounts reached 60.1 million

Streaming Hours increased by 14.4 billion hours YoY to 73.2 billion

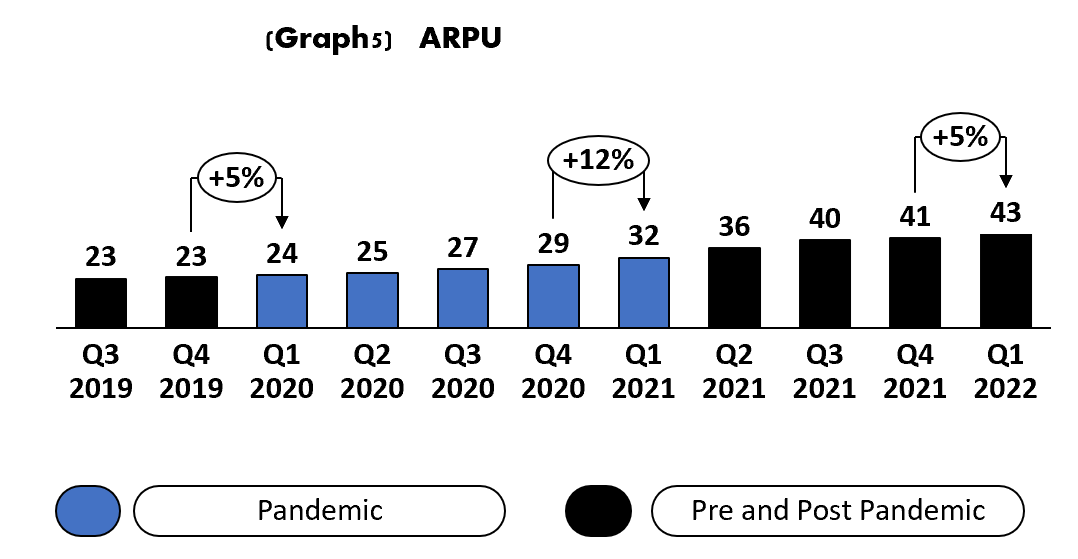

Average Revenue Per User (ARPU) grew to $41.03 (trailing 12-month basis), up 43% YoY

No. 1 TV streaming platform in the U.S., Canada, and Mexico by hours streamed

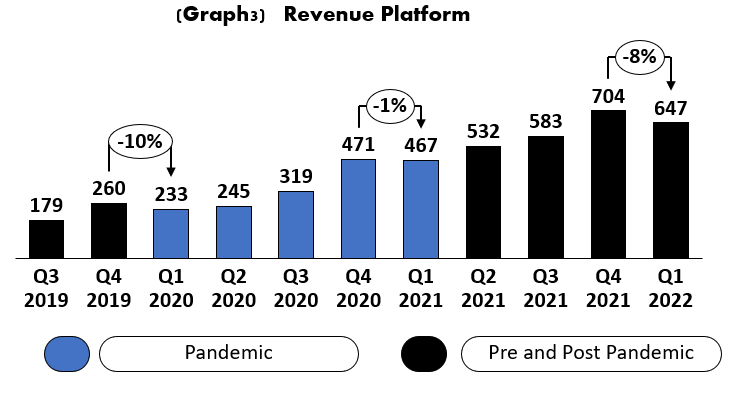

During Q1 2022, revenue has come down both for platform and player. This tends to be seasonal, Q4 is a quarter when both advertisers and also consumers spend a lot more.

The drop between Q1 2022 and Q4 2021 is 15%, the drop between Q1 2021 and Q4 2020 was 12%. When looking at previous years in 2021 and in 2019, the seasonal drops in both revenue streams have been similar, with the exception of the end of 2020. That was in the middle of one of the worst waves of the pandemic, hence a lot of people stayed home and streamed a lot during that time.

The drop in revenue in Q1 2022 had additional impacts from supply chain issues of TV manufacturers. Global supply chain disruptions have impacted the U.S. TV market. Some of Roku TV OEM partners were hit particularly hard with inventory challenges, which negatively impacted their unit sales figure. Q2 is being guided at $805m in revenue, $395m in gross margin and breakeven in Ebitda. This continues to be impacted by supply chain issues.

Over the years there has been an impressive improvement in ARPU. Remember that they are mainly just a platform, yet they have reached a trailing 12 months ARPU of $42.9. That would be about $3.58 in revenue per month per active subscriber. Gives a lot to think about considering that they produce very little content yet manage to get a lot of revenue out of each active account.

Other improvements have been seen in active accounts and streamed hours. Streaming hours are very important, since the more hours, the more possible impressions that could generate advertising revenue for Roku.

Streaming hours per active account are currently at about 3.8 hours per day per account, this is lower than the average TV time for an average US household, which is close to 8 hours.

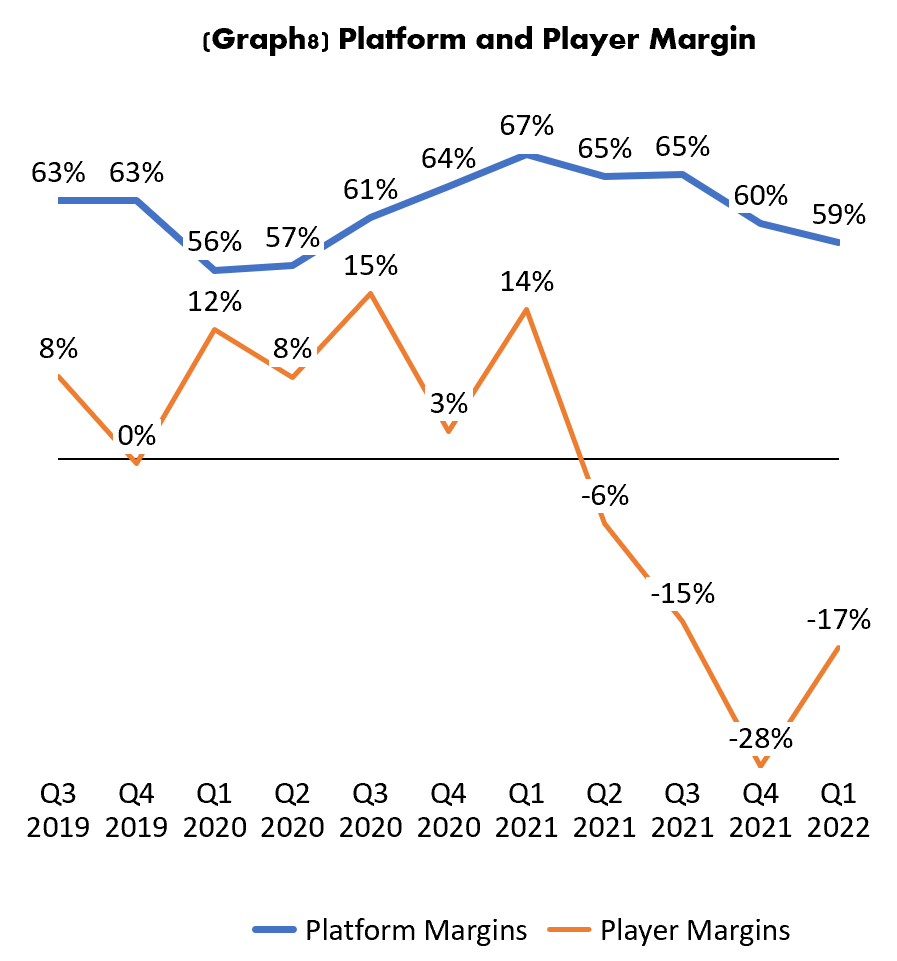

On the margins side, there is a great difference between the margins for players and the platform. Margins for platform are very high (though have been reduced in the last few quarters) they have average between 59% to 65%, while player had average about 8% before supply chain issues, the last 12 months come down to -17%. Roku has addressed this and said that they are doing everything possible to have as much inventory as possible, things like having air shipping and negotiating with chip manufactures. They are committed to avoiding passing the incremental cost to customers, they want to keep prices stable and connect more customers. Margins for players are expected to be impacted until the supply chain normalizes.

It is in Roku’s interest to keep adding homes to their ecosystem, even if they have a negative margin on the players, the lifetime value of that customer will end up being positive (when considering an annual ARPU of $43). This just translates into the cost of acquiring customers.

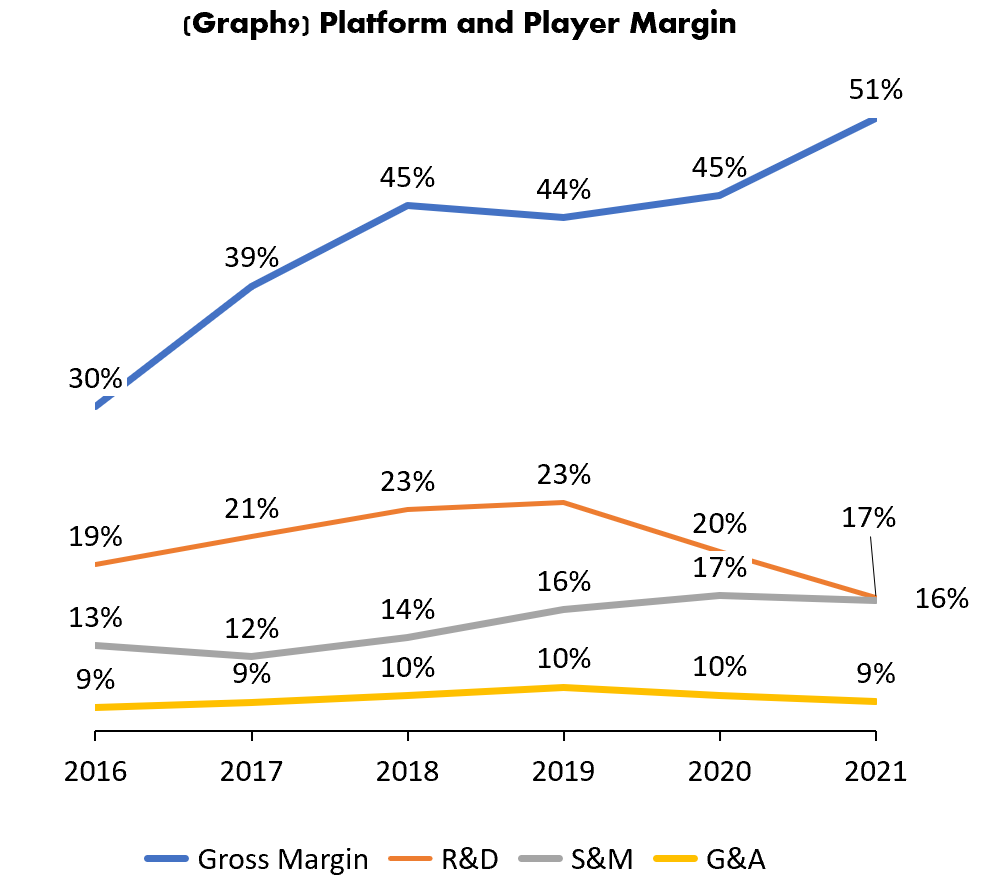

When looking at the OpEx and its historic performance, we can clearly see that the platform margins have helped greatly in taking overall gross margin from 30% in 2016 to 51% in 2021. This is mostly due to the platform becoming a bigger part of the revenue. They represented about 25% of the revenue in 2016 while they already make 82% of the revenues in 2021. We could expect in the long term that margins will look similar to platform margins (slightly below)

Both sales and marketing and G&A have kept growing relatively at the same pace as revenue. R&D has come down as a percentage of revenue but they have mentioned in their earnings calls that 2022 will be a year of bigger investments. They reduced spending in 2020 and 2021 to prepare for the uncertainty of the pandemic. That in the end could have been a sneak peak on how their margins will improve when they finalize investing for growth. For now, Roku is ‘‘all in’’ on continuing to establish the platform.

Balance Sheet

Roku currently holds $2.2b in cash, this is a wonderful cushion considering that they are even starting to show signs of profitability. When it comes to debt they also don’t have a great amount of debt. They hold $132m in current debt and $444m in long term debt, for a total of $576 m in debt.

Elsewhere, Capex has been historically low, has averaged $56 m the past few years and $51m in the last 12 months.

Streaming Wars and Rokus role in it

Rokus has been smart enough and has placed itself as an impartial player of the ‘‘streaming wars’’. A few years ago, it was basically only Netflix, today, there are many more players entering the business. All of them are battling for a limited amount of dollars in the customer’s pocket. This will likely generate many changes to the world of streaming, the world of streaming in 2015 and the world of streaming for the next 5 years and beyond are, and will, be very different.

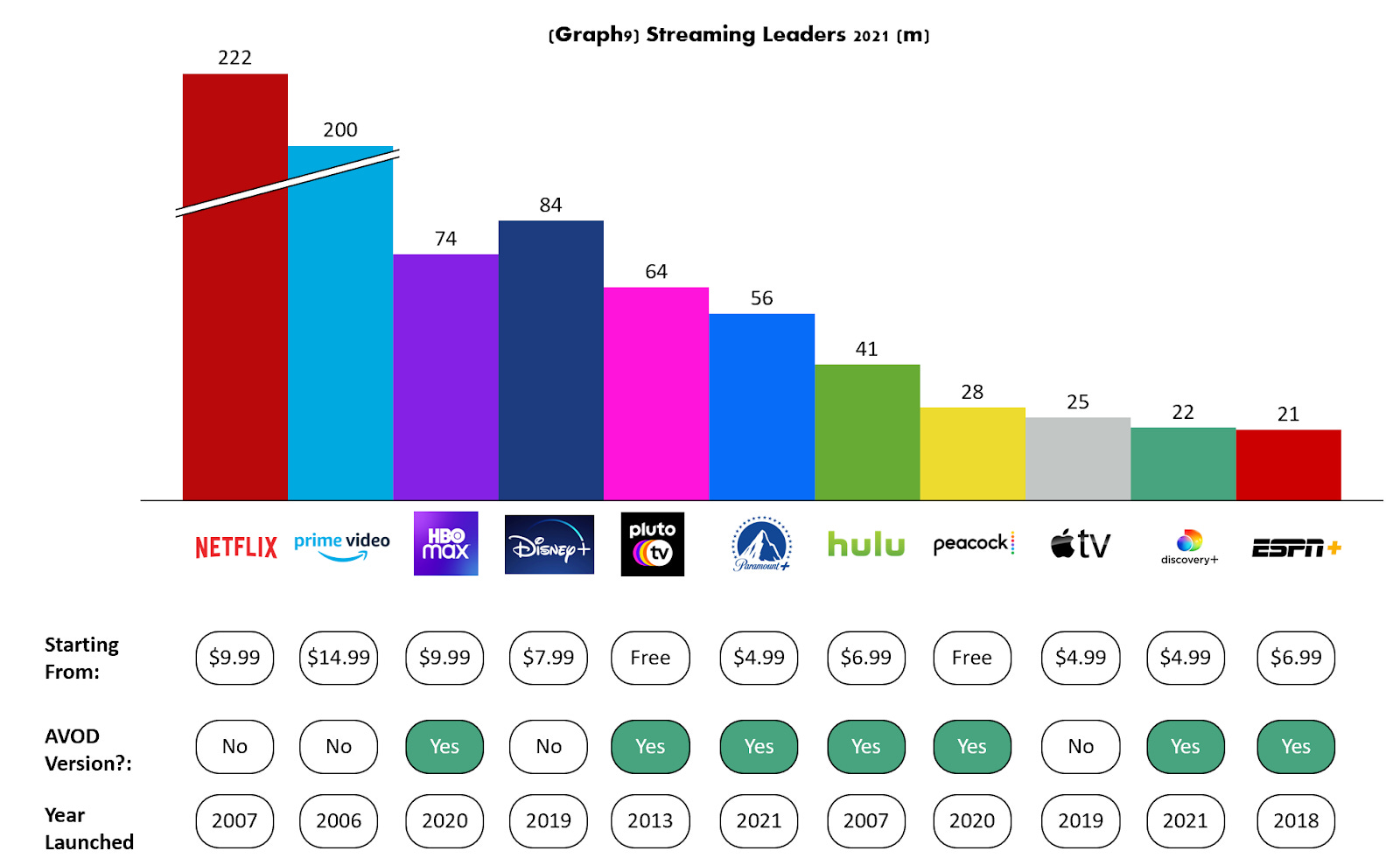

Streaming TV is starting to trend towards AVOD (Advertising based video on demand) Just as an all out war started, the new entrants are adding entry plans with an AVOD option. It has even been announced that Netflix will have an AVOD version soon. This does not come as a surprise, for example, let's assume a household contracted all of the products from the graph below, it takes over $85 if you have all of them without ads! That amount of money is no longer a ‘’deal’’ or affordable for consumers. This creates a new subscriber behavior, one that jumps from one service to another. This is likely the reason why the new entrants, almost all of them, come with a cheaper ad supported version. It is not sustainable financially for all these content providers to continue producing large amounts of content if the churn for each service will accelerate. It was a far simpler world before where the competition was very small (Hulu, Netflix , Amazon) but now that there are many players this large investments in content will have to be financed with the help of advertising.

For the customer, this becomes more attractive, they still want to watch the content, but don’t want to pay a huge amount of money for something that they will not use every day

The opportunity for Roku here is just starting, they can profit well from being the platform. The one that works with these publishers of content and without making huge investments in content

So far they have taken advantage already, remember that under platform revenue they also have subscription revenue. Basically they get a percentage of the subscription that is done on their platform, this is similar to IOs where Apple takes about 30% of any monthly subscription on their platform. We don’t know exactly the percentage for Roku(it is definitely different with each content owner), but it might be about 20% of each monthly subscription. Having many content providers launched in the past 3 years, it is likely that they have been accumulating these subscriptions via Roku since then.

Roku is the number one TV OS in the country and has started expanding to other countries internationally. They have the negotiating power to have advertising and subscription revenues from these content providers as long as they keep being the leading OS.

Read our other material on:

Opendoor Peloton Carvana Rivian

Size of the opportunity

First of all, it is clear that content production is starting to focus solely on the streaming channels. Traditional linear TV is being left with only live sports, for now, there is a clear trend that live sports will come out of traditional TV. MLS has announced that it will go to Apple TV + next year, MLB Baseball is starting to have games also on Apple TV +, the NFL Sunday Ticket is rumored to move to streaming only next year. Amazon Prime already has NFL Thursday night Football, European Champions league is part of Paramount +, Spanish La liga of ESPN+, etc. As soon as live sports comes out of linear TV, the traditional cable services will be left out with only old and unattractive content. This will happen by design, content providers are investing heavily in streaming content and not in linear content. As soon as this happens, the channel grids of Pluto TV, Tubi, Frevee and others will look fairly similar to what traditional cable providers can offer. These types of services called FAST (Free Ad supported Streaming TV) will gain influence rapidly. Roku Channel will (and it is already doing it) play in this section of the market.

Traditional cable has to pivot somewhere else, Generation Z and Millennials are not the typical cable subscribers, they are the typical cord cutters. The demographic group from 18 to 49 years old already spends more time streaming than they do watching traditional TV. It seems that Comcast has identified the trend and it is focused on delivering a box included for free to internet only subscribers (called Flex) this box is their own platform and will play the game Roku is playing (advertising and aggregator of subscriptions) They even have partnered recently with Charter to license and continue to grow the Flex ecosystem, and in the processes trying to establish themselves as a platform as well.

Currently streaming penetration is 46% of time spent on a TV, this market will go for 100% streaming, that does not mean 100% on demand content, there will be linear content available, but that will be streamed as well. That is why the platform or OS is very important. Previously we have seen similar platform battles. We saw it in computers, where Windows and Apple ended up being the winners. In the world of Smartphones, there was a lot of fragmentation before the iPhone, every single brand had their own OS. But since then everything has been consolidated to Android and iOS, and those are money machines for both of them.

The largest screen in the home had been highly fragmented as well. There are still many players in this field. The are large deep pocketed players like Amazon (Fire Stick), Apple (Apple TV) and Google (Android TV). Yet Roku has proven that it can play with these giants and currently leads the US, Canada and Mexico market as the number one platform.

With this huge changes in TV coming, migration to streaming and growth in AVOD content, Roku expects that TV advertising budgets will move to streaming platforms. Currently only 18% of the advertising budgets are being spent on streaming and the rest still being spent in traditional linear TV. Total US traditional TV advertising is estimated to be currently $60 b and worldwide something around $200b. With sports coming out of linear TV this likely will go to close to 100% streaming fast in the next 5 years.

So the opportunity for the winning platforms is very big. It is estimated that the world will reach a long term target of 1 billion streamers, budget for advertising will move here, and it will be a $200b plus opportunity in advertising and as well an opportunity in continued revenue stream from subscription revenue sharing with content providers. All of this pie will likely be shared between platforms and content providers, it is just an evolution of the cable model, where content providers and cable providers share the revenues. The cable provider will be now replaced by the TV platforms. It is a reshuffling of players, similar to the music industry, where CD distributors and stores were killed, replaced by music platforms where all music is shared (Spotify, Apple Music, Amazon Music, YouTube Music pretty much the same players as in TV and one outlier that is the leader, Spotify is the Roku of Music)

Competitive Landscape:

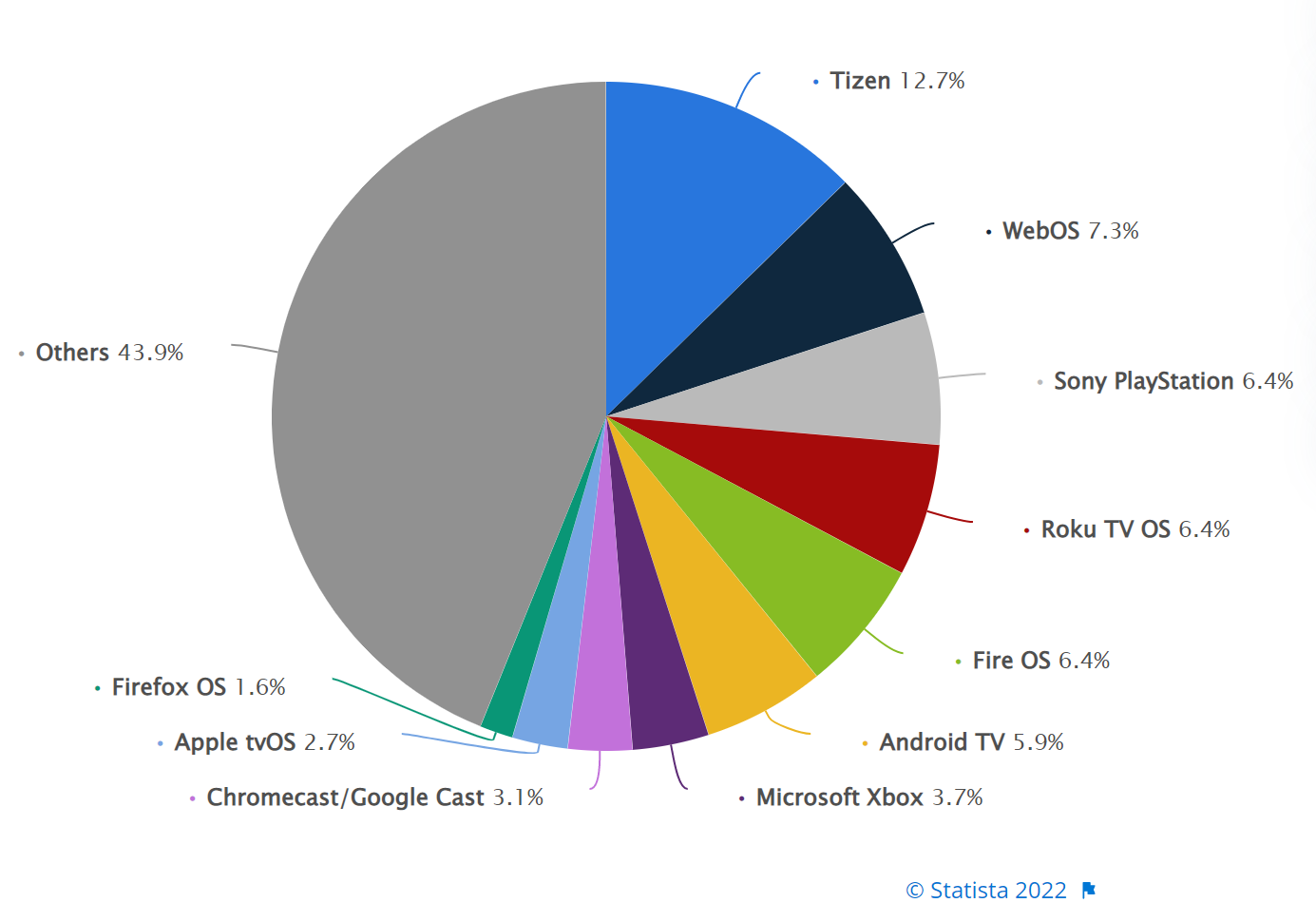

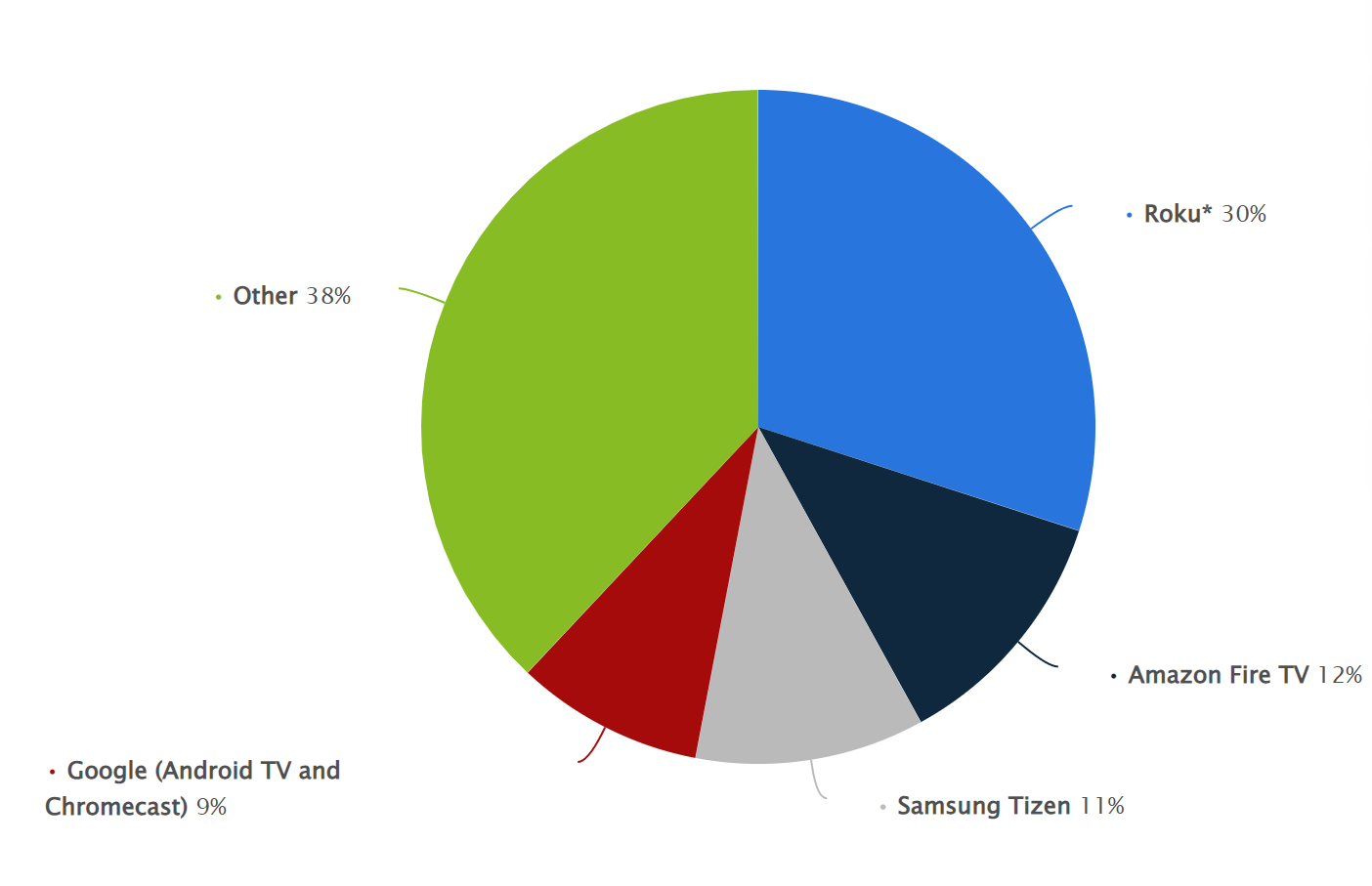

Roku is the leading OS in the US, but worldwide still does not have a very big presence. From the graph below we see that they have about 6% of the market worldwide and LG ((WebOs) and Samsung (Tizen). (and a huge fragmented ‘‘others’’ bucket as well)

Smasung has used Tizen in wearables, cameras and some smartphones. Tizen OS has been included in Samsung TVs since 2015. Tizen is not something that Smasung is fully focused on though, they announced already that smartwatches from 2021 will no longer use Tizen (they are switching to Android). As of now they will continue to use this OS for their TVs. But when comparing their TV OS to others, the experience from Tizen is less attractive than others, so they might decide later to switch to another OS for their TVs. It is likely that they would go to Android, given the many other uses of Android in Samsung devices.

WebOs is the evolution of the software developed by HP. LG acquired the OS and is now being used on their TVs. It is also not better quality versus players like Apple, Android, Roku or Fire. But similar to Samsung, their TVs are probably the best quality out there and some of the best sellers. They both are the leaders in OS not because of their great OS, but of the great TVs.

If these two players remain in the game as platforms (Samsung and LG) they will have a place for sure in the discussion.

In the US they (Roku) are the leaders, but as seen below, there are still many “others”, the market seems to be highly fragmented and only about 70% are in established platforms. We expect that in the coming years, as TVs are replaced in households, this will converge to only about 3 or maximum 4. The key here for Roku, or any other platform, is to get as many TV manufacturers to build with their OS. Android, Roku and Amazon Fire are all trying the same game. LG and Samsung will probably leave this game, these two are about hardware and not software, so whoever gets on board with these manufacturers will establish itself as the leader long term. Google here is well positioned, they have already done LG TV products (not necessarily TVs, but boxes used by i.e LG telecom) and they have very close relation with Samsung.

Some of the possible risks for the company are:

Late to international: They could be late to gain international market share. They are starting with Latin-American. But Asian and European markets could be conquered by other players if they don’t invest in these places soon.

AVOD market does not grow: If we are not correct, and the migration to a AVOD focused market is rejected by the customers, a great amount of possible opportunities will have a great impact on the overall opportunity for these platforms.

Tempted by Streaming Wars: They could be tempted into investing a huge amount of money into the production of its own content. If they do, they would kill one of their best attributes, the one of being an impartial player in the war between content providers. This is the thing that could hold back Amazon Fire for example. If Roku invests heavily here, they likely will eat away immense amounts of resources, they are late to the war and they are small compared to others. They have announced already that they will invest in its own content, but hopefully, it is just small investments to attract households to the Roku channel.

Creating their own TV: Another mistake that could endanger their neutrality. They are better as the OS provider than fighting with a huge amount of Asian TV manufactures. If they get into a war with them, they might lose important contracts that they have today, and would rely only on TV sticks.

What could be the case for Roku being a good opportunity for the next 10 years?

Big Market: from the naked eye the market might look small for Roku. But an increased amount of content supported by advertising could help Roku become the YouTube of TV platforms. The place where advertisers want to come to do business because of its quality and stickiness.

Profitable Scale: Their revenue comes from products with very good margins and very little capital investment, once they reach a mature platform the margins could improve a lot and the cashflow coming from it could be very big

It is still very early: The migration to streaming is still very early. The streaming war has been going on for about 4 to 5 years. But once it settles the amount of streamers in the world will be very large. It will be even more popular than cable. Cable was more of an American thing, streaming will be a worldwide phenomenon and as mentioned above, we expect that the platforms will take the place of the cable operator.

Valuation

Roku currently is valued at $11.6 b or $85.77 per share, as many other companies it has dropped by a huge amount in the past 12 months (82%). It has many positive things going for them. Very strong balance sheet, good performance and a low cash burn, this makes it a lot easier to get a fundamental DCF analysis.

Base Case: In this scenario Roku continues to grow its active account base, it grows their ARPU but not aggressively, their device sales continue somewhat stable with no considerable changes. In this scenario the company would be valued at $99.76 per share or $13.5b

Conservative Case: In this scenario the active base grows slower and ARPU remains flat similar to the devices. In this scenario margins also are expected to be lower. In this scenario the company would be valued at $43.72 per share or $5.93b

Optimistic Case: In this scenario base and ARPU grow at a faster pace, the device market is not that different from the base case. Margins are a little better. In this scenario the company would be valued at $139.36 per share or $18.9b

In the base case and optimistic scenario we get a better valuation than current market value. In the conservative case we would need deteriorating margins on the advertising side to have it come to fruition. Roku's opportunity is very big, they saw the future of the streaming war before most, and they have positioned themselves in the best spot to cruise and grow through the battle.