Uber reported Earnings this past Tuesday beating expectations convincingly with $8.07b in revenue vs a consensus of $7.39b. The stock reacted very positively by closing Wednesday up 18.9%. The company reported a large loss, but like we mentioned in our piece from a few weeks ago, Uber is highly distorted at the net income level due to participation that it has in other companies. This is why it is better to look at operating income. Net income looks ugly from a quick glance, but we will walk you through the quarter to explain the positive reaction by the market.

Thanks for reading LongYield! Subscribe for free to receive new posts and support my work.

Performance Summary:

Revenue

Revenue was $8.07b for the quarter, up 105% YoY

Revenue was also higher by 2.48 times Q1 2020, one of the last quarters with smaller impact from the pandemic.

Total Gross bookings were $29b up 33% YoY

Mobility Gross bookings were $13.3b, up 54.6% YoY and 24.6% MoM

Mobility Revenue was up 119.7% YoY and 41% MoM

Mobility take rate was 26% considerably above the 18.7% they had in Q2 2021 ( Take rate is revenue divided by gross bookings)

Delivery Gross bookings were $13.8b, up 7.4% YoY and down 0.19% MoM

Delivery Revenue was up 36.9% YoY and 7% MoM

Delivery take rate was 19.4% above the 15.2% they had in Q2 2021

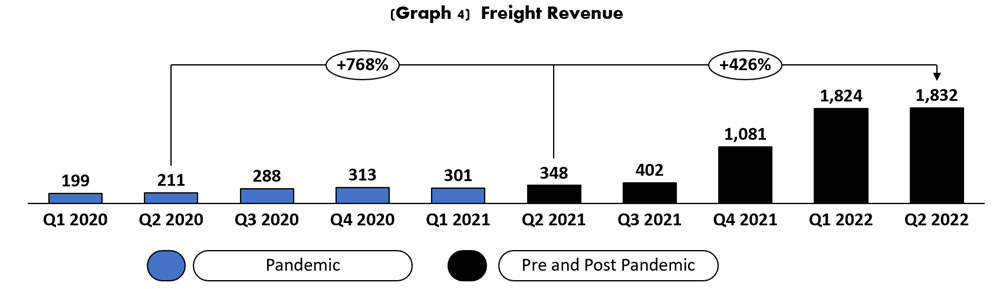

Freight revenue was up 426% YoY, yet MoM was barely 0.43% up

When looking at their revenue by region compared to Q4 2019 (pre pandemic) the US is 2 times larger, EMEA and APAC 3.5 times while Latam is still lagging and is only 90% the size it had in Q4 2021

Key Metrics:

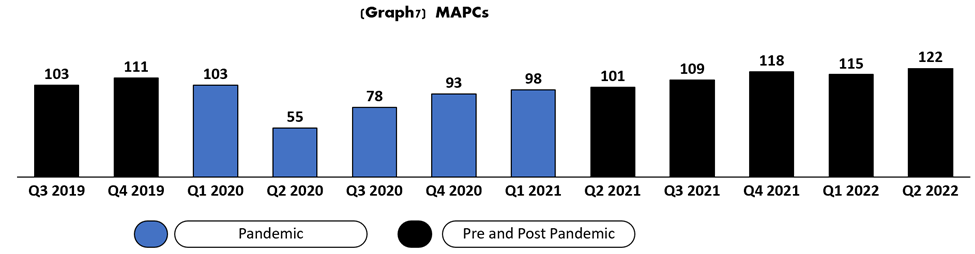

- MAPCs grew to 122m in the quarter up 21% YoY and 6% MoM (MAPCs is the number of unique consumers who completed a Mobility ride or received a Delivery order on the platform at least once in a given month, averaged over each month in the quarter)

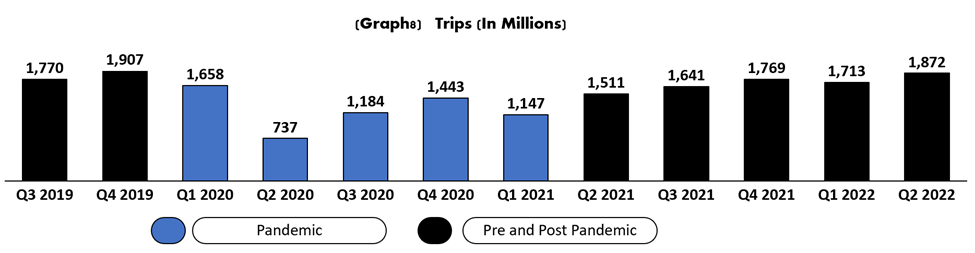

- Trips grew to 1,872m in the quarter up 24% YoY and 9% MoM (Trips are the number of completed consumer Mobility rides and Delivery orders in a given period)

- They have reached 10m Uber one Subscribers.

Cost and Expenses:

- Operating Income for the quarter was -$649m a smaller loss than Q2 2021 by $505m but larger than Q1 by $167m

- Cost of goods sold were $5.1b or 64% of revenue worse than previous quarter and same quarter last year (59% and 53% respectively)

- Cost of goods grew vs same quarter last year mainly due to:

o $1.3 billion increase in Freight carrier payments and incentives resulting from the acquisition of Transplace in the fourth quarter of 2021

o $835 million increase in Driver payments and incentives that are recorded in cost of revenue, exclusive of depreciation and amortization, because of business model changes in the UK

o $411 million increase in insurance expense primarily due to an increase in miles driven in our Mobility business

o $364 million increase in Courier payments and incentives that are recorded in cost of revenue for certain markets where we are primarily responsible for Delivery services and pay Couriers for services provided

- Operations and Support grew 43% YoY, but it now is just 8% of revenue vs 11% the previous year

- Sales and Marketing decreased by 3% YoY and went down from 32% as a percentage of revenue to just 15% showing great improvement in scale

- Sales and Marketing decreased $38 million primarily attributable to:

o Decrease in consumer discounts, rider facing loyalty expense, promotions, credits, and refunds of $74 million to $553 million compared to $627 million in the same period in 2021 and

o $22 million decrease in consumer advertising expenses

o The decrease was partially offset by a $46 million increase in employee headcount costs.

- Research and Development increased by 44% but also showed great scale by reducing its percentage of revenue from 16% to 11%

With improvements in both S&M and R&D Uber showed great improvements in scale on its way to profitability, all its costs combined went from 130% in Q1 2021 to 109% in Q2 2022, it is through, a small setback from the previous quarter, were the total expenses were 107%. The issue here continues to be the cost of revenues, as mentioned above is the one that grew considerably for the quarter. This means that the new growth is coming with a worse operating leverage or that they are getting back mobility growth at worse margins.

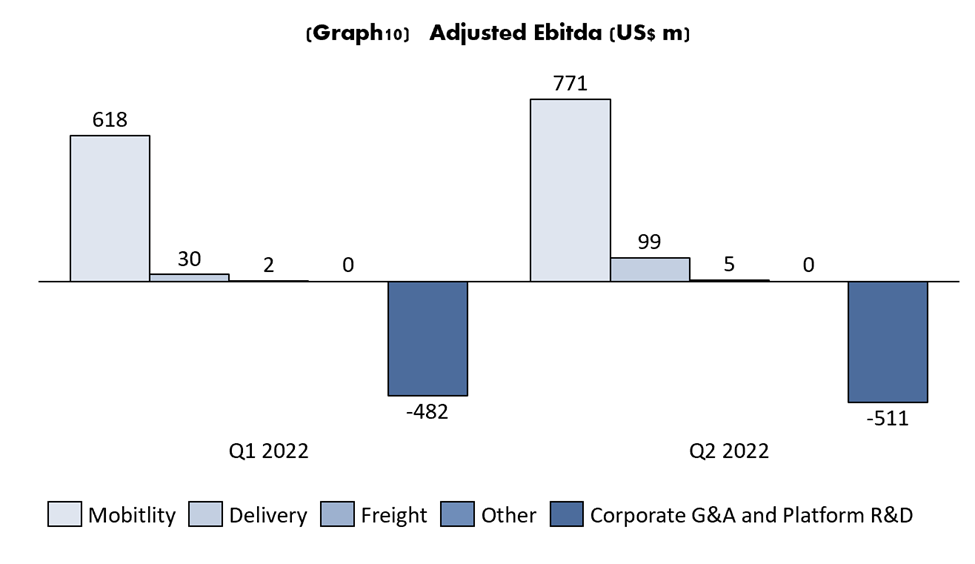

When looking at what Uber shows as “Adjusted Ebitda” the company also showed great improvements, even profitability overall, but like we mentioned in our previous article, you always must be skeptical of what is shows as adjusted Ebitda.

All three segments of Uber’s business showed positive Adjusted Ebitda, this is the second quarter in a row, this time also higher than previous quarter, it went from 168m in Q1 to 364m in Q2.

Thanks for reading LongYield! Subscribe for free to receive new posts and support my work.

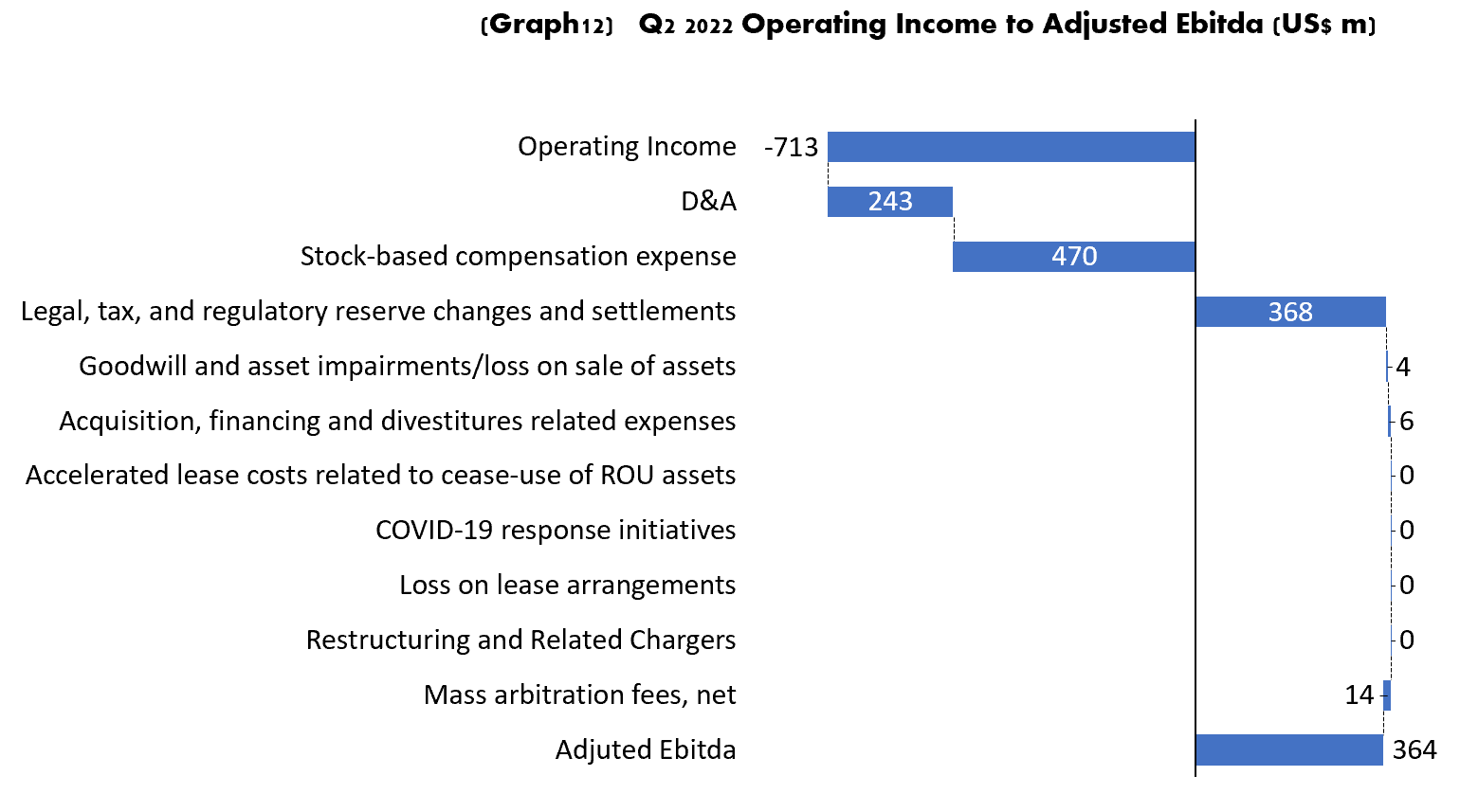

Again, we will prefer to go in detail on what they are excluding in their adjusted Ebitda rather than just take their word for it. Before all distortions from big revaluations for participations in Aurora, Grab, Zomato, Uber had a negative operating income of $713m. This is probably the cleanest number from their performance in Q2. This is for the fourth quarter in a row one of the better quarter for Uber in term of profitability, it went down due to the increase in the increase in costs of revenues, but their improvements in scale for S&M and R&D if consistent should take them to positive operating income if revenue continues to grow.

Once again, this quarter some of the bigger components that took the company to negative operative income were non-cash, for example depreciation and amortization at $243m and Stock based compensation at $470m (a jump from $359 in Q1 2022) considering the size of the company in terms of current market cap this makes small dents in terms of dilution, so it is actually a good way to use their stock as currency and save cash.

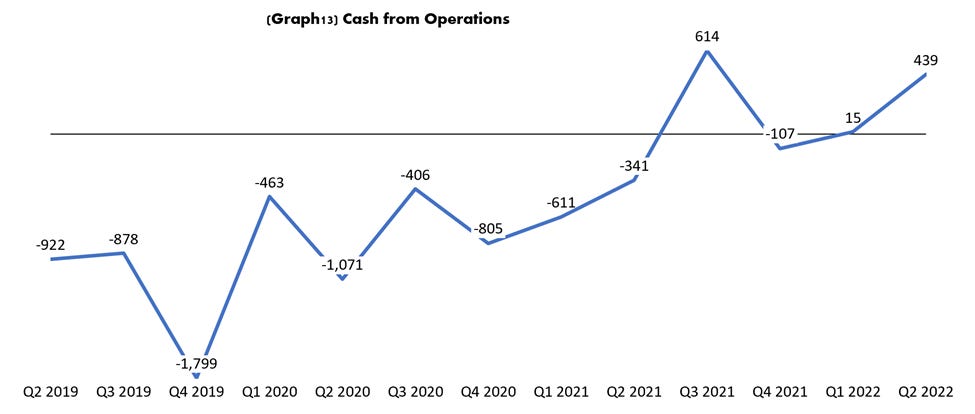

Cash from operations was actually very positive this quarter, the business generated $439m in cash, up from $15m in cash the previous quarter. This is a major achievement from Uber, it is starting to generate positive cash flow consistently from their operations alone. It is only the third time that they manage to do it, but the second consecutive time. This is one of the most positive signs that Uber might be close to real positive operating income (Q3 2021 is distorted due to sale of investments, so actually the last two would be two only positive quarters if we exclude this quarter)

Balance Sheet

- Cash and cash equivalents went up from $4.18b to $4.39. This is another major milestone; this is the first time it happens without any major issuance of stock (exc. Stock compensation) or any issuance of new debt.

- Long term debt remained flat, third quarter in a row that remains around $9.7b

- Total debt, including capital leases (short and long) and long-term debt, decreased by $227m from $11.42b to $11.19b

Operational highlights

Uber has been getting back slowly to pre pandemic levels on many operational points in their business. It has gotten an improvement in wait times, it went from 7.4 minutes at its worst in 2021, to 4.5 minutes now, but still far from their pre pandemic level of 2.8 minutes. In the US, the amount of trips getting ‘’surged’’ has gone from 39% at its worst to 14% now, as well, still above their pre pandemic level of 6% ( surged: price increase when there is little supply of drivers)

This shows that on the mobility side they still might be lacking some drivers. Yet they claim that this will likely improve in the coming months. First, because they are having better result on onboarding drivers, they have the advantage that they can onboard “earners” from the delivery side of their business. Second, inflation might help them recruiting people. Inflation is hurting a lot of people and more people are looking for “side hustles’’ to make additional money to take on the impact of inflation.

On the Uber one membership they have seen their base grow to 10 m customers, they have launched this service in 7 markets globally. In the markets that they have launched, 23% of the gross bookings are coming from members, and when looking at delivery specifically this is higher at 32%, for delivery, Uber one subscription increase engagement by 2.7 times vs the gross booking of non-members.

Outlook

Uber is a different company today than what it was before the pandemic. It is actually a far stronger company. Most would have never thought that this would be the case. Most would have expected that the company would be close to being out of business after seeing quarters with operating income of many negative billions of dollars. Yet the verticals are growing, delivery and freight became key components that helped the company to become the platform the management many times has told us that they intend to be. This platform environment, or this ecosystem as we like to call it, might be the reason why they will be the leader for years to come in this industry. The fact that they operate in both mobility and delivery gives them major competitive advantage from competitors like Lyft, Doordash, Rapi, Pidelo Ya, Glovo etc. Uber most continue to be focused on their Uber One product; the subscription offering will be in the end the difference maker. The advantage of being able to offer both services (mobility and delivery) combined will make them stronger in the long term. The benefit from having unlimited delivery and discounts on rides is very attractive to many customers. Once these customers are subscribed, they will be inside the platform (or ecosystem) and economically for customer will be very difficult to get out of there. Doordash cannot compete with this without having to suffer on their margins with great discounts on delivery, Lyft cannot compete because they cannot offer the same benefits only on the mobility side. There are many small players in the industry, many for them wont’s survive, and consolidation will happen. Uber will be one of the big ones and other mobility and delivery services will consolidate. But this is good for Uber. Competition will consolidate, the markets will have fewer players so financial performance will be far healthier that it is today in an environment of a lot of small players, these small money losing players will go broke and consolidate (and Uber might be the one sole global player)

In terms of valuation, their performance in Q2 is in line with the expected performance in our base model. We continue to believe that currently their right valuations is $36 (so getting very close to the $32 is trading today). They have shown the path to profitability, but they are not quite there yet. How many quarters will it take for them to be profitable is the big question. For now, the best thing and one of the big reasons why the market took so well their results, is that they are having positive cash flow from their operations. Even when taking into account investments in Property plant and equipment. Looks like Uber will be here to stay.

Thanks for reading LongYield! Subscribe for free to receive new posts and support my work.

The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained on our substack constitutes a solicitation, recommendation, endorsement, or offer by LongYield or any third party service provider to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction.